AI illustration of key proposals in the Finance Bill 2026./GEMINI

AI illustration of key proposals in the Finance Bill 2026./GEMINI

Tax amnesty, mobile phone levy changes and betting tax among key proposals explained

Audio By Vocalize

AI illustration of key proposals in the Finance Bill 2026./GEMINI

The National Assembly has unveiled the key proposals contained in the Finance Bill, 2026, setting the stage for debate on a package of tax measures aimed at raising revenue, improving compliance and streamlining tax administration.

The Finance Bill is one of the government's main tools for financing public expenditure. The National Assembly says taxes collected under the proposed framework help fund roads, healthcare, education, water projects, electricity, security, public sector salaries and repayment of public debt.

The extensive legislative proposal introduces crucial amendments to the country's tax frameworks. The government presents this bill during the Fifth Session of the Thirteenth Parliament to reshape public revenue collection and economic compliance.

The introduction of the bill aligns with Section 39A of the Public Finance Management Act, Cap. 412A. Every year, the National Government introduces a Finance Bill to amend tax laws in order to raise revenue for funding national development and public services. The funds collected through taxation go directly toward supporting key public amenities and national obligations. These resources are used to finance roads, healthcare, education, water projects, electricity, security, salaries for public servants, and repayment of public debt.

The massive bill seeks to overhaul a wide array of existing laws. It proposes various amendments to Kenya’s tax laws, specifically targeting the Income Tax Act, the Value Added Tax (VAT) Act, the Excise Duty Act, the Tax Procedures Act, the Miscellaneous Fees and Levies Act, the Stamp Duty Act, and the Road Maintenance Levy Fund Act.

According to parliament, the main objective of the Finance Bill, 2026, is to raise additional revenue and to enhance tax compliance. Lawmakers also state that the Bill seeks to seal tax loopholes, simplify tax procedures, and align Kenya's tax system with international and modern business practices. This comprehensive explainer provides a detailed breakdown of what the proposed law contains, what it changes, and what it leaves untouched.

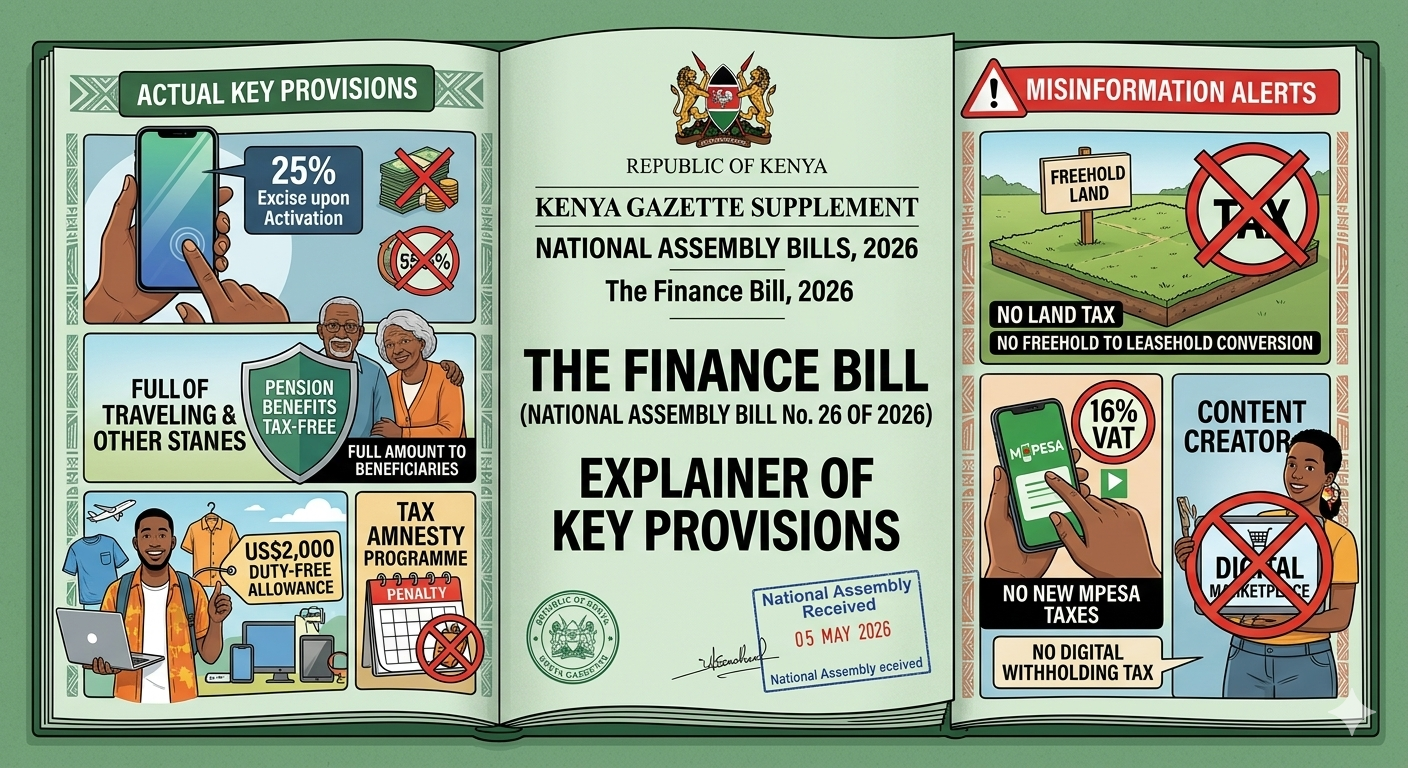

The proposed bill contains significant tax relief measures aimed at supporting families and boosting specific business sectors. One major social relief involves the protection of retirement benefits for bereaved families. The Bill proposes that pension benefits paid to dependants or beneficiaries of a deceased pension scheme member will not be subject to income tax. Under the proposal, upon the demise of a pension scheme member, the money paid to their spouse, children, or dependants will be exempt from tax. This ensures that the beneficiaries will receive the full amount of the benefits without deduction.

To boost the property sector, the bill introduces a critical waiver to encourage collective property investment. The Bill proposes to exempt property transfers to Real Estate Investment Trusts (REITs) from Capital Gains Tax (CGT). Parliament defines REITs as investment trusts that allow people and companies to invest collectively in real estate projects such as commercial buildings, apartments, shopping malls, and housing developments.

Currently, when property owners transfer property into a REIT, they may be required to pay CGT on the increase in the value of the property. The proposed amendment seeks to remove this tax burden to encourage additional investments in REITs and shall promote the growth of the real estate industry.

One of the most notable changes in the bill alters how mobile devices are taxed, moving the tax point to the network connection. Currently, when a mobile phone is imported into Kenya, excise duty is payable immediately at the point of importation, regardless of whether the device is ever sold or used. Similarly, for phones manufactured locally, excise duty becomes due at the time a device is released from the factory. Under the proposed amendment, excise duty will no longer be payable at importation or upon release of a device from the factory. Instead, the tax will become due only when the phone is activated on a mobile network.

The National Assembly clarifies that mobile phones face heavy taxation at the border under the old framework. Devices are currently subject to multiple domestic taxes and levies during importation, including 16% VAT, 10% Excise duty, 25% Import duty, 2.5% Import Declaration Fee, and 2% Railway Development Levy. Together, these amount to approximately 55.5% under the current mobile phone taxation framework.

The state explicitly clarifies that "the proposal in the Finance Bill, 2026 does not introduce a new tax on Mobile Phones." Instead, the amendments simplify the existing structure by replacing the current framework with a single 25% excise duty collected upon activation of a phone.

The digital economy is also facing new tax compliance measures. The Bill proposes to introduce VAT on certain digital and platform-based financial services. These services include payment processing services, payment gateways, digital transaction platforms, merchant acquiring services, aggregation services, and other technology-based financial systems provided for a fee or commission.

The bill introduces a stricter tax stance for regional investors and gaming enthusiasts. For East African Community (EAC) investors, the bill removes a long-standing tax benefit. Currently, citizens and companies from EAC countries enjoy a reduced withholding tax rate of 5% on dividends earned from investments in Kenya. The explainer reminds readers that dividends are profits that a Company distributes to its shareholders.

The Bill proposes to remove this special treatment and apply the normal withholding tax rate of 15% to all non-residents, including EAC citizens and companies. Consequently, investors from countries such as Uganda, Tanzania, Rwanda, Burundi, and South Sudan will now pay 15% withholding on dividends earned from Kenyan investments.

The gaming sector will also experience higher tax deductions. The Bill proposes to introduce a 20% withholding tax on betting and gaming winnings for both residents and non-residents. If passed, individuals who win money from betting, gaming, lotteries, or gambling activities will have 20% deducted before receiving their winnings. Additionally, a 5% excise duty will continue to apply to money deposited into betting wallets and gaming accounts. The document notes that the measures seek to protect and guard the public against the social impacts of betting and gambling while ensuring revenue collection.

For corporate entities, specifically card merchants, the definition of certain transaction fees will change. The Bill proposes to define interchange fees and merchant fees paid by Card Merchants as "management or professional fees". Card Merchants such as banks, fintechs and payment service providers pay fees to payment networks such as Visa and MasterCard to use their networks. The classification means that Card Merchants are required to withhold and remit a portion of the fees as withholding tax.

The bill also adds software distribution to the tax net. It proposes to include the distribution of a software where regular payments are made for the use of software through the distributor in the definition of "royalty" for purposes of collection of withholding tax on the fees.

The petroleum and mining industries face mixed changes under the new bill. Foreign mining and oil companies will see a new tax on profits sent out of the country. The Bill introduces a 15% tax on profits repatriated outside Kenya by mining and petroleum companies operating in the country. This means that when foreign companies transfer profits earned in Kenya back to their parent companies abroad, they will first pay tax in Kenya.

Conversely, petroleum contractors will get a significant tax reduction. The Bill proposes to reduce the corporate income tax rate for non-resident petroleum contractors from 37.5% to 30% to attract much-needed investment in the petroleum sector.

On domestic trade, the bill tightens invoicing and hire purchase systems. To expand the tax net, the bill targets all businesses regarding documentation. The Bill proposes that all persons supplying goods or services will now be required to issue invoices. This proposal is aimed at improving record-keeping, enhancing tax compliance, and increasing transparency in business transactions, and it will enhance efficiency for small businesses.

Furthermore, hire purchase rules are being tightened to prevent revenue leakage. The Bill proposes that only businesses licensed under the Hire Purchase Act will be allowed to exclude financing charges when calculating VAT. Currently, many businesses selling goods on hire purchase terms can separate the cost of the product from the financing cost when calculating VAT. The National Assembly notes that this was not the intended purpose of the benefit and is subject to abuse unless amended.

The tourism sector and international travelers are also directly affected by the new provisions. For tour operators, the rules for tax exemptions will become stricter. The Bill proposes that only tour operators licensed by the relevant tourism authority will qualify for VAT exemptions. It also seeks to define what qualifies as "in-house supplies" in the tourism sector.

In contrast, international travelers will enjoy a massive increase in their tax-free shopping allowance when arriving in Kenya. Currently, travellers returning to Kenya are allowed to bring goods worth up to USD500 into the country without paying VAT. The Finance Bill, 2026, proposes to increase this duty-free allowance to USD2,000.

This change means travellers will now be able to bring in higher-value personal goods without paying VAT, significantly increasing the tax-free threshold.

The proposal is intended to reflect current economic realities, inflation, and the increasing cost of goods globally. Providing a specific scenario, the document notes that a Kenyan returning from abroad with a laptop, mobile phone, clothing, and personal electronics worth Ksh. 250,000 shall be allowed to enter the country without paying VAT on those items.

The bill lists several goods and services that will be completely exempt from the 16% Value Added Tax. This is aimed at lowering costs for manufacturing, green energy, transport, and health. The Bill proposes VAT exemptions on several goods, including:

Certain Dialyzers, which are critical components of dialysis machines.

Scrap metal.

Worn clothing and other worn articles, other than upon importation (Mitumba).

Transportation of sugarcane from farms to milling factories.

The supply of imported or locally purchased telephones for cellular networks and other wireless networks.

The supply of motorcycles of tariff heading 8711.60.00.

The supply of electric bicycles.

The supply of solar and lithium-ion batteries.

The supply of electric buses of tariff heading 87.02.

Bioethanol vapour (BEV) Stoves classified under HS Code 7321.12.00 (cooking appliances and plate warmers for liquid fuel).

Major infrastructure projects will also receive tax relief under the new law. The bill excludes VAT on the supply of goods and services for the direct and exclusive use in the implementation of approved infrastructure projects undertaken under a public-private partnership framework. The document states that removing VAT on these projects will reduce construction costs and encourage more private investors to participate in infrastructure development. Lower taxes may make such projects more financially attractive and easier to implement.

The Bill also proposes separate VAT exemptions on goods and services used directly in approved Public-Private Partnership (PPP) infrastructure projects. Public-Private Partnerships involve collaboration between the government and private investors to finance and develop public projects such as roads, airports, water systems, and energy infrastructure.

Taxpayers with outstanding debts have an opportunity to clear their records under a new relief programme. The Finance Bill, 2026, proposes to reintroduce a tax amnesty covering all tax liabilities accrued up to 31st December 2025. This follows the expiry of the previous tax amnesty programme on 30th June 2025, which had covered taxes owed up to 31st December 2024.

Under this proposal, taxpayers who had already paid their principal taxes by 31st December 2025 will automatically qualify for a waiver of penalties and interest without making a formal application to the Kenya Revenue Authority (KRA). For instance, if a business had unpaid penalties and interest on taxes from previous years but fully cleared the main tax amount by 31st December 2025, the penalties and interest may be cancelled automatically.

However, those who still owe principal taxes must take proactive steps. Taxpayers who still have outstanding principal taxes as at 31st December 2025 will be required to apply to KRA and enter into a payment plan. The payment arrangement must ensure all outstanding principal taxes are fully paid by 31st December 2026 in order to qualify for the waiver of penalties and interest. These amendments are part of the proposals to enhance the ease of doing business in Kenya.

While offering an amnesty, the bill simultaneously strengthens the collection powers of the tax authority. The Finance Bill, 2026, proposes changes to the powers of KRA in issuing agency notices to recover unpaid taxes. An agency notice is a legal instruction issued by KRA directing a third party, such as a bank, employer, customer, tenant, or business partner holding money on behalf of a taxpayer, to remit the money directly to KRA to recover tax arrears.

The proposal seeks to strengthen tax enforcement and improve recovery of unpaid taxes from taxpayers who fail to settle their obligations. The state emphasizes that the amendment shall enhance recoveries from taxpayers who deliberately avoid paying taxes despite having access to funds through banks, customers, or other business arrangements.

A significant portion of the official document focuses directly on addressing public anxiety and debunking false information circulating online regarding the content of the bill. The National Assembly explicitly notes that "some members of the public and stakeholders have based their submissions on FAKE VERSIONS of the Bill circulating online and have responded to non-existent provisions." To ensure public consultations are accurate, members of the public and stakeholders are strongly advised to access the "ACTUAL VERSION" of the Finance Bill, 2026 from the official Parliament website.

To settle public concern, the National Assembly has issued a direct disclaimer: "CONTRARY TO FALSE REPORTS circulating in sections of the media and social media," several widely discussed clauses are completely non-existent. The document formally outlines five key clarifications regarding land, digital content, rent, and mobile money:

First, the Finance Bill, 2026 "DOES NOT contain any amendments to existing land laws and does not impose any tax or burden on freehold land."

Second, the National Assembly clarifies that "it is UNTRUE that the Finance Bill, 2026 contains any provision proposing to convert freehold land to leasehold land."

Third, the text states that the Finance Bill, 2026 "DOES NOT IMPOSE Withholding tax on Digital Content Monetisation or Digital Marketplace transactions."

Fourth, the statement clarifies that the Finance Bill, 2026 "DOES NOT increase the existing resident rental income tax." Instead, the Bill simply proposes to treat rental income earned by non-resident landlords as a final tax upon payment of a 30% withholding tax on the gross rental income received.

Fifth, the government firmly rejects rumours regarding mobile money transaction taxes, stating that "it is UNTRUE that the Finance Bill, 2026 intends to impose a 16% VAT or any other additional taxes on M-Pesa transactions."

Help us continue bringing you unbiased news, in-depth investigations, and diverse perspectives. Your subscription keeps our mission alive and empowers us to provide high-quality, trustworthy journalism. Join us today to make a difference!

![[PHOTOS] Red carpet in Pretoria as Ruto begins South Africa visit](https://cdn.radioafrica.digital/image/2026/06/abe3e750-6e5a-4394-a45c-899768be6240.jpeg)